Table of Content

- Header

-

ENROLLMENT

- ELIGIBILITY

- HOW TO ENROLL

- QUALIFYING LIFE EVENTS

- EMPLOYMENT STATUS CHANGES

- LAST DAY OF COVERAGE & COBRA

- RATES

-

BCBS MEDICAL

- Medical Plans

- Summary of Benefits and Coverage (SBC)

- VIRTUAL VISITS

- LEARN MORE

- PHARMACY

- RX COST SAVINGS

- EXTRAS

-

UHC MEDICAL

- Medical Plans

- VIRTUAL VISITS

- Summary of Benefits and Coverage (SBC)

- PHARMACY

- RX COST SAVINGS

- UHC APP

- LEARN MORE

-

CIGNA MEDICAL

- Medical Plans

- Summary of Benefits and Coverage (SBC)

- VIRTUAL CARE

- CIGNA MOBILE APP

- LEARN MORE

- PHARMACY

-

AETNA MEDICAL

- Medical Plans

- Summary of Benefits and Coverage (SBC)

-

KAISER MEDICAL

- Medical Plans

-

CURATIVE MEDICAL

- Baseline Visit

- Medical Plan Options

- Summary of Benefits and Coverage (SBC)

- VIRTUAL VISITS

-

SPENDING ACCOUNTS

- HEALTH SAVINGS ACCOUNT (HSA)

- HSA pt.2

- HEALTH REIMBURSEMENT ACCOUNT (HRA)

- FLEXIBLE SPENDINGS ACCOUNT (FSA)

- LIMITED PURPOSE FSA (LPFSA)

- DEPENDENT CARE FSA (DCFSA)

-

MOO DENTAL

- Dental Plan

-

EYEMED VISION

- Vision Plan

-

SURVIVOR BENEFITS

- VOL LIFE AND AD&D

- PORTABILITY & CONVERSION

-

INCOME PROTECTION

- LTD

-

REIMBURSEMENT

- ACCIDENT

- CRITICAL ILLNESS

- HOSPITAL INDEMNITY

- ANSEL

- ansel pt2

-

ASSISTANCE

- COMPSYCH EAP

- UNUM EAP

- TELUS EAP

- UHC EAP

- SUPPORTLINC EAP

- MENTAL HEALTH

- INSURCHOICE

- NATIONWIDE PET INSURANCE

- WISHBONE PET INSURANCE

- UNUM TRAVEL ASSISTANCE

- IDENTITY THEFT

- LEGAL SERVICES

- INDIVIDUAL LIFE INSURANCE

- LEGAL

- 401(k)

-

RESOURCES

- CARRIER CONTACTS

- MEDICARE ELIGIBLITY

- GLOSSARY

- REQUIRED NOTICES

- FREQUENTLY ASKED QUESTIONS (FAQs)

- Footer

ELIGIBILITY

HOW TO ENROLL

All team members have access to our online benefits enrollment platform 24/7 where you have the ability to enroll, select or change your benefits online during the annual open enrollment period, new hire orientation, and for qualifying events.

- Accessible 24/7;

- View all benefit plan options and your elections;

- View important carrier forms and links;

- Report a qualifying life event; and

- Make changes to beneficiary designations and more.

ENROLLMENT INSTRUCTIONS [Any additional info/codes they should know?]

- Go to add enrollment link

- Enter your User ID: Email Address

- Enter your Password

- Follow instructions and enroll in your benefits

- Make sure to save a copy of your confirmation statement and enrollment forms.

To get started, click on the link below to head to your enrollment portal!

QUALIFYING LIFE EVENTS

Under certain circumstances, employees may be allowed to make changes to benefit elections during the plan year, if the event affects the employee, spouse, or dependent’s coverage eligibility. Any requested changes must be consistent with and on account of the qualifying event.

Examples Of Qualifying Events:

- Legal marital status (for example, marriage, divorce, legal separation, annulment);

- Number of eligible dependents (for example, birth, death, adoption, placement for adoption);

- Work schedule (for example, full-time, part-time);

- You, your spouse, or other covered dependent become enrolled in Part A, Part B, or Part D of Medicare

- Death of a spouse or child;

- Change in your child’s eligibility for benefits (reaching the age limit);

- Becoming eligible for Medicaid; or

- Your coverage or the coverage of your Spouse or other eligible dependent under a Medicaid plan or state Children’s Health Insurance Program (“CHIP”) is terminated as a result of loss of eligibility and you request coverage under this Plan no later than 60 days after the date the Medicaid or CHIP coverage terminates; or

- You, your spouse or other eligible dependent become eligible for a premium assistance subsidy in this Plan under a Medicaid plan or state CHIP (including any waiver or demonstration project) and you request coverage under this Plan no later than 60 days after the date you are determined to be eligible for such assistance.

A status change from part-time to full-time is not a qualifying event, but it is a change in eligibility that will allow an employee to enroll in insurance.

- Newly eligible employees will have 30 days to enroll in insurance benefits, which will begin on the first day of the month after the employee has completed 60 days of full-time employment.

- Reminder, this means working 30+ hours per week for 60 days.

A status change from full-time to part-time will cause employees to become ineligible for insurance benefits.

- The insurance benefits will end on the last day of the month before the status change becomes effective.

- A termination will also cause an employee to lose their benefit at the end of the month the employment ended.

- Both of these situations will trigger eligibility for continuing coverage under COBRA.

[insert COBRA admin logo]

COBRA Customer Service | insert phone number | insert URL

The Consolidated Omnibus Budget Reconciliation Act (COBRA) gives workers and their families the right to continue their existing group health plan coverage for a limited period of time when they would otherwise lose their coverage through a voluntary or involuntary job loss, a reduction in work hours, death, divorce, or other events.

The cost for coverage under COBRA is usually higher than the cost for employees under a group plan.

- COBRA participants usually pay 100% of the coverage, plus a 2% administrative fee.

- For employees who choose not to re-enroll in benefits during Open Enrollment, the loss of insurance coverage is not a qualifying event for COBRA.

Cobra Qualifying Events

The following are qualifying events for covered employees if they cause the covered employee to lose coverage:

- Termination of the employee's employment for any reason other than gross misconduct.

- Reduction in the number of hours of employment.

The following are qualifying events for the spouse and dependent child of a covered employee if they cause the spouse or dependent child to lose coverage:

- Termination of the covered employee's employment for any reason other than gross misconduct.

- Reduction in the hours worked by the covered employee.

- Covered employee becomes entitled to Medicare.

- Divorce or legal separation of the spouse from the covered employee.

- Death of the covered employee.

In addition to the above, the following is a qualifying event for a dependent child of a covered employee if it causes the child to lose coverage:

- Loss of dependent child status under the plan rules.

- Under the Patient Protection and Affordable Care Act, plans that offer coverage to children on their parents' plan must make the coverage available until the adult child reaches the age of 26.

RATES

[INSERT RATES]

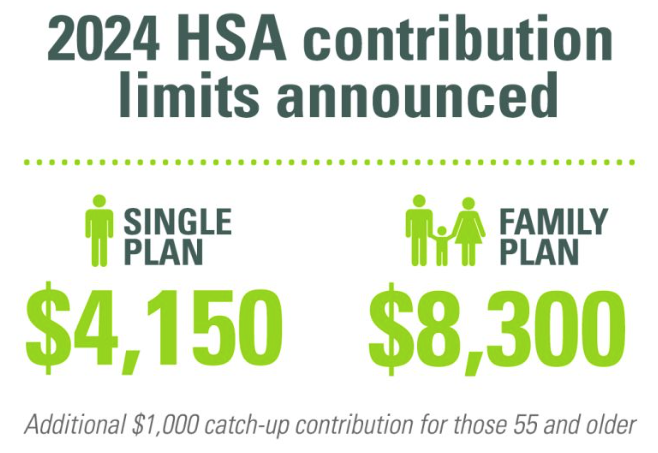

HEALTH SAVINGS ACCOUNT (HSA)

A Health Savings Account (HSA) is a tax-advantaged personal savings account that can be used to pay for medical, dental, vision and other qualified expenses now or later in life. To contribute to an HSA, you must be enrolled in the BCBS HSA $3,200 Plan and your contributions are limited annually.

Visio Lending contributes $750 (Employee) / $1,500 (Family) to your HSA on a per pay period basis.

How It Works

- For 2026, Participants can make an annual election of up to $4,400 for self only HDHP coverage or $8,750 for family High Deductible Health Plan (HDHP) medical coverage.

- Your employer deducts per pay-period the amount you elect on a tax-free basis. You can also contribute post-tax contributions (up to the maximum allowed) and recognize the same tax savings by claiming the deduction when filing your annual taxes.

- Eligible healthcare purchases can be made tax-free when you use your HSA. Purchases can be made directly from your HSA account, either by using your debit card, online bill-pay, or check – or you can pay out-of-pocket and then reimburse yourself from your HSA.

- The interest on HSA funds grows on a tax-free basis, and interest earned on an HSA is not considered taxable income when the funds are used for eligible medical expenses.

Why Participate? HSAs save you money!

- The contributions you make to an HSA are deducted from your paycheck on a pre-tax basis – before federal income, social security, and most state taxes.

- The end results of your HSA contributions is a lower taxable income, and a tax advantaged vehicle to pay for out-of-pocket healthcare expenses and prepare for your healthcare costs in retirement.

- While your funds can be used to pay for immediate healthcare expenses tax-free, you can also save the money for healthcare expenses later in life.

- You can continue to contribute year after year and withdrawals (provided you are enrolled in an HDHP) can be made at any point in time.

- Whether you withdraw the money tomorrow, five years from now, or in retirement, funds used for qualified healthcare expenses are always tax-free.

Who's Covered?

- An HSA covers qualified out-of-pocket expenses for you, your spouse, your tax dependents, even if they are not covered under an HDHP.

FLEXIBLE SPENDINGS ACCOUNT (FSA)

Rippling Customer Service | (850) 425-4000 | www.rippling.com

An FSA is an account your employer sets up so you can pay for a variety of healthcare needs, like insurance co-pays, deductibles, dental, vision, pharmacy and even some over-the-counter medication costs, reimbursed under the Health FSA.

Why Participate?

- Reduce taxable income – FSA Contributions are deducted from your paycheck on a pre-tax basis, so they lower your reported annual income, resulting in lower taxable wages.

- Save on healthcare expenses – Using pre-tax funds to pay out of pocket expenses can save you hundreds!

- Offset rising healthcare costs and individual financial responsibility.

Maximum Annual Contribution

- For the 2026 plan year, the Healthcare FSA contribution limit is $3,400 per employee.

Grace Period

- Visio Lending offers a grace period for FSA spending. You have 2½ months after the plan year ends on December 31, 2026 to incur additional expenses and submit them for reimbursement. Therefore, any remaining balance in the previous plan year that ended December 31, 2026 will be used to pay that grace period expense even though the service was provided in the NEW plan year.

- The grace period applies to both the Dependent Care and Healthcare FSAs.

Eligible Expenses

- A full list of qualified FSA expenses can be found in IRS Publication 502 at www.irs.gov.

- You can learn more about FSA qualified expenses and also make purchases by visiting the FSA Store at www.fsastore.com.

DEPENDENT CARE FSA (DCFSA)

Rippling Customer Service | (850) 425-4000 | www.rippling.com

A Dependent Care FSA (DCA) is a reimbursement program that allows you to set aside pre-tax funds to help pay for qualified dependent care expenses. Most participants use this program to pay for child daycare and after-school care expenses; however, it can be used to pay for adult daycare expenses as well. It serves as an alternative to using the Dependent Care Tax Credit. Funds can only be used on a dependent child under the age of 13 or dependents who are unable to care for themselves. Unlike a Flexible Spending Account, DCA funds can only be used as they are deposited into your account.

Maximum Annual Contribution

- For the 2024 plan year, you can contribute up to $5,000 ($2,500 if married and filing separately).

Eligible Expenses

- You may be reimbursed only for care that enables you to work, go to school full-time, or look for work on a full-time basis. DCA funds can be used on expenses such as tuition for licensed daycare facility, preschool, after-school programs, elder care, summer day camps, and in-home dependent care services.

MOO DENTAL

Mutual of Omaha Customer Service | (800) 775-6000 | www.mutualofomaha.com

Network: Mutually Preferred Network

How do I find an In-Network Dentist?

- Use the helpful link below or visit your provider’s website at www.mutualofomaha.com where you can search by provider/center name or search by location.

Did You Know?

- You have the freedom to select the dentist of your choice; however, when you visit a participating in-network dentist, you will have lower out-of-pocket costs, no balance billing, and claims will be submitted by your dentist on your behalf.

Pre-treatment Estimate

- If your dental care is extensive and you want to plan ahead for the cost, you can ask your dentist to submit a pre-treatment estimate. While it is not a guarantee of payment, a pre-treatment estimate can help you predict your out-of-pocket costs.

Looking for more details about how items are covered? Click on the links below to view the formal Benefit Summary.

EYEMED VISION

Network: EyeMed Insight Network

How do I find an In-Network Provider?

- Use the helpful link below! In-Network providers can also be found at www.eyemed.com under the "Member & Consumers" tab, then select "Find An Eye Doctor." Your vision plan utilizes the Insight Network.

- Staying in-network helps you save money on eye exams, frames and lenses. Visiting a PLUS Provider is designed to help you save even more. And since PLUS Providers are already in-network, the additional perks are built right into your vision benefits. No promo codes, no coupons, no paperwork. The same vision benefits, plus a little more savings.

Did You Know?

- Eyes can give doctors a clear picture of overall wellness. That’s why vision care—and vision benefits—can help employees stay healthy. A comprehensive eye exam can detect early signs of serious health problems, such as diabetes, heart disease, high blood pressure, high cholesterol, glaucoma and cataracts

Looking for more details about how items are covered? Click on the link below to view the formal Benefit Summary.

SURVIVOR BENEFITS

Mutual of Omaha Customer Service | (800) 775-6000 | www.mutualofomaha.com

Basic Life and Accidental Death & Dismemberment (AD&D)

Life insurance is an important part of your financial security as it helps protect your family from financial risk and sudden loss of income in the event of your death. AD&D (Accidental Death & Dismemberment) insurance is equal to your Life benefit in the event of your death being a result of an accident, and may pay benefits for particular injuries sustained.

Basic Life / AD&D insurance is a company paid benefit, provided to you at no cost. The plan pays a flat benefit of $10,000. Keep in mind, your life insurance benefit amount will reduce to 65% of the original amount at age 65 and to 50% of the original amount at age 70. See your plan summary below for more details.

Voluntary Life and AD&D

In addition to your employer provided Basic Life insurance coverage, you have the opportunity to enroll in Voluntary Life and AD&D Insurance. Coverage is also available for your spouse and/or child dependents, however, It is required that you elect coverage for yourself in order to elect coverage for your dependents.

If you have previously elected Voluntary Life but are under the Guarantee Issue (GI) amount, you may increase your amount up to the Guarantee Issue (GI) without Evidence of Insurability (EOI) at Open Enrollment. If you previously waived Voluntary Life you will need to submit Evidence of Insurability (EOI).

How does it work?

- You choose the amount of coverage that’s right for you, and you keep coverage for a set period of time, or “term.” If you die during that term, the money can help your family pay for basic living expenses, final arrangements, tuition and more. AD&D Insurance is also available, which pays a benefit if you survive an accident but have certain serious injuries. It pays an additional amount if you die from a covered accident.

Who can get Voluntary Term Life Coverage?

- Employee: Choose from $10,000 to $500,000 in $1,000 increments, up to 5 times your earnings. You can get up to $180,000. This is the amount of coverage you can qualify for with no medical underwriting.

- Spouse: Get up to $500,000 of coverage in $1,000 increments. Spouse coverage cannot exceed 100% of the coverage amount you purchase for yourself. Your spouse can get up to $35,000 with no medical underwriting, if eligible.

- Children: Get up to $10,000 of coverage in $1,000 increments if eligible (see delayed effective date). One policy covers all of your children until their 26th birthday. The maximum benefit for children live birth to 6 months is $1,000.

Guaranteed Issue (GI) and Evidence of Insurability (EOI)

- When you are first eligible (at hire) for Voluntary Life and AD&D, you may purchase up to the Guaranteed Issue (GI) for yourself and your spouse without providing proof of good health (EOI).

- Any amount elected over the GI will require EOI. If you elect optional life coverage and are required to complete an EOI, it is your responsibility to complete the EOI and send to the provider. In addition, your spouse will need to provide EOI to be eligible for coverage amounts over GI, or if coverage is requested at a later date.

Life insurance portability and conversion options are features that allow policyholders to maintain some level of insurance coverage when they might otherwise lose it or wish to change the type of coverage they have.

Portability

- Refers to the ability of an individual to transfer their group life insurance coverage from one employer to another or from a group policy to an individual policy without undergoing new underwriting or providing evidence of insurability.

- This is commonly associated with group term life insurance provided by employers. If you (the employee) leave your job or retire, you may not want to lose your life insurance coverage, especially if there are ongoing health issues. Advantages of porting coverage are that it allows continuity of coverage and there is no need for medical examination or evidence of insurability.

- The application and check for the initial premium must be received within 31 days after Life Insurance terminates or 15 days from the date the Employer signs the application; whichever is later.

Conversion

- The Conversion option allow you to convert your term life insurance policy into permanent (e.g., whole life or universal life) insurance policy without providing evidence of insurability or undergoing new underwriting. Transitions from term to permanent coverage without having to do a new medical exam.

- This option is considered when an individual has ongoing health issues or may be unable to qualify for a new policy.

- An Insured Employee and Dependent(s) may convert Group Voluntary Life Insurance coverage, without evidence of insurability, to an Individual Life Insurance policy during the 31 day period following termination of employment.

How do I port or convert my coverage?

- Contact your employer’s HR department for the applicable portability and/or conversion forms. You can also call your carrier customer service at (800) 775-6000 or access the forms at www.mutualofomaha.com.

It's essential for policyholders to consider the options available to you and request conversion or portability timely, within 30 days of your benefits termination. You will submit the request for conversion or portability directly to the insurance carrier and will set up direct payment for your new individual policy.

INCOME PROTECTION

Mutual of Omaha Customer Service | (800) 775-6000 | www.mutualofomaha.com

Short-Term Disability

Everyday illnesses or injuries can interfere with your ability to work. Even a few weeks away from work can make it difficult to manage household costs. This employer-paid Short Term Disability coverage provides financial protection for you by paying a portion of your income, so you can focus on getting better and worry less about keeping up with your bills.

- Elimination Period - Benefits begin on the 8th day of an injury or illness.

- Benefit Duration - Payments may last up to 12 weeks (You must be sick or disabled for the duration of the waiting period before you can receive a benefit payment).

- Coverage Amount - The policy pays 60% of your weekly income up to $1,500 per week until the employee returns to duty or has been disabled for up to 25 weeks; whichever occurs first. This is an employee paid benefit.

What does this mean to you?

- If you are out of work for 7 days due to an illness or accident, you can begin receiving disability benefits on day 8. This is a cash benefit of 60% of your weekly salary to a max of $1,500 when you are out of work. You are able to receive this benefit for up to 12 weeks. A partial cash benefit is available if you can only do part of your job or work part-time.

Long-Term Disability

This employer-paid coverage pays a monthly benefit if you have a covered illness or injury and you can't work for a few months - or even longer! You're generally considered disabled if you're unable to do important parts of your job - and your income suffers as a result. This benefit is provided to you at no cost!

- Elimination Period- Benefits begin on the 90th day of an injury or illness.

- Benefit Duration - Payments may last up to Social Security Normal Retirement Age (SSNRA) (You must be sick or disabled for the duration of the waiting period before you can receive a benefit payment).

- Coverage Amount - Covers 50% of your monthly income, up to a maximum benefit of $10,000 per month.

- 3/12 Pre-existing Condition: If you have a medical condition that begins before your coverage takes effect, and you receive treatment for this condition within the three months leading up to your coverage start date, you may not be eligible for benefits for that condition until you have been covered by the plan for 12 months.

What does this mean to you?

- If you are still unable to work after your Short Term benefit expires, you will have the opportunity to receive a Long Term Disability cash benefit. Starting on the 90th day you are out of work due to an illness or injury, you will receive 50% of your monthly salary to a max of $10,000. It will continue to pay you a benefit until age 65, your Social Security Normal Retirement Age or 3.5 years, whichever is longest. This benefit is provided at no cost to you.

REIMBURSEMENT

Accident Insurance

A serious injury can cost you a lot of money – not only in medical bills but in things like income from lost work hours. Accident insurance is a robust shield against the unpredictable, safeguarding you against the financial fallout of unforeseen injuries. It pays a set benefit amount based on the type of injury you have and the type of treatment you need, ensuring that whether you face minor bruises or major medical emergencies, you're covered. Here's what accident insurance typically covers:

- Comprehensive Coverage: This plan covers accidents like broken bones, severe burns, and emergency room visits.

- Medical Expenses: It helps offset expenses related to ambulance rides, hospital admissions, surgeries, therapy, and other necessary treatments.

- Income Protection: Should an injury result in lost work hours, accident insurance provides a financial safety net to help bridge the gap until you're back on your feet.

With accident insurance in your corner, you can face life's uncertainties with confidence, knowing that you're financially protected against the unexpected. However, it's important to note that accident insurance typically excludes coverage for routine check-ups or hospitalization due to illness. Additionally, injuries sustained prior to purchasing the accident insurance plan are not covered. For a detailed breakdown of benefits and coverage, refer to the plan summary provided below.

Critical Illness Insurance

Facing a critical illness can bring not only physical strain but also financial burdens due to medical expenses and potential loss of income. Critical illness insurance serves as a robust safety net in such challenging times, offering financial protection against the unforeseen. In the event of a critical illness diagnosis, this insurance provides a lump-sum payment to the insured individual, enabling them to cover various expenses, including medical treatments, mortgage payments, and daily living expenses. Here's what critical illness insurance typically covers:

- Coverage for Various Conditions: Critical illness insurance typically covers a wide range of serious medical conditions, including cancer, heart attacks, strokes, organ transplants, and more. Visit your plan summary below to learn how different illnesses are covered.

- Financial Assistance: The policy provides a lump-sum payment upon diagnosis of a covered critical illness, allowing individuals to use the funds as needed for medical expenses, household bills, or other financial obligations.

- Flexibility and Peace of Mind: With critical illness insurance, employees gain peace of mind knowing they have financial protection in place, regardless of the specific illness they may face. This flexibility ensures that they can focus on their health and well-being without worrying about the financial consequences of a critical illness.

While critical illness insurance provides invaluable protection against serious medical conditions, it's essential to note that the plan typically excludes pre-existing conditions diagnosed before the policy's effective date, as well as certain illnesses not specified in the plan. Additionally, routine check-ups and hospitalization due to non-critical illnesses are typically not covered. For a comprehensive understanding of the benefits and limitations of your specific plan, be sure to review the plan summary provided below.

Hospital Indemnity Insurance

Even if you have medical insurance, a trip to the hospital can leave you with significant unexpected expenses. Hospital indemnity insurance is a valuable addition to your benefits package, providing financial protection in the event of hospitalization due to illness or injury. This insurance offers a fixed daily benefit amount for each day you're hospitalized, helping offset expenses not covered by your primary health insurance, such as deductibles, copayments, and other out-of-pocket costs. It serves as a financial safety net, ensuring that you can focus on your recovery without worrying about the financial impact of a hospital stay. Here's what hospital indemnity insurance typically includes:

- Daily Hospitalization Benefit: You receive a fixed cash benefit for each day spent in the hospital, providing financial assistance to cover various expenses incurred during your stay. You can receive benefits when you’re admitted to the hospital for a covered accident, illness, or childbirth. See the full list in the plan summary below.

- Flexibility in Use: The benefit can be used at your discretion to cover costs like deductibles, copayments, transportation, and even household bills while you're unable to work.

While hospital indemnity insurance offers valuable financial support during hospitalization, it's important to note that it typically excludes coverage for pre-existing conditions and certain elective procedures. Additionally, benefits may not be payable for hospital stays due to specific causes, so be sure to review the plan summary below for more information on coverage details and limitations. Your understanding of the plan specifics will empower you to make informed decisions about your healthcare coverage.

MENTAL HEALTH: ADDITIONAL RESOURCES

Call 911 if you or someone you know is in immediate danger or go to the nearest emergency room.

988 Suicide & Crisis Lifeline

- Dial 988 to be connected with 24/7/365 emotional support.

- Free, confidential crisis counseling, including appropriate follow-up services, is available no matter where you live in the United States.

War Vet Call Center

- Veterans and their families call 877-WAR-VETS (877-927-8387) to talk about their military experience and/or readjustment to civilian life.

INSURCHOICE

InsurChoice offers you the ability to personalize your protection program — bringing you quick, convenient, holistic coverage with incredible cost-saving discounts across a variety of top-rated insurance products and carriers. Our program is simple, fast, and always online. Find coverage in the blink of an eye!

Key benefits include:

- Competitive pricing: One size doesn’t fit all, so you can match yourself with the best rates and coverages from multiple insurance companies.

- Custom-tailored coverage: Select the products that meet YOUR needs.

- Stability: We have relationships with key national carriers who have a proven track record of rate and coverage stability.

- Innovation: With our innovative product delivery platform we are constantly striving to add more benefits and improve your experience.

Click the link below to receive your FREE no obligation quote customized especially for you!

LEGAL SERVICES

INDIVIDUAL LIFE INSURANCE

Life insurance provides financial protection for survivors of the insured, and may meet other financial objectives, as well. Families should review their life insurance program and policies regularly and make adjustments to meet changes in circumstances and needs. Please reach out to Shayne Eddleman to schedule an appointment.

Shayne Eddleman

(512) 914 – 0113

LEGAL

Customer Service | (800) 252-9346 | texaslegal.org

Always Have Legal Help When You Need It

Texas Legal has experienced and qualified attorneys to serve our members in multiple practice areas. We have the most comprehensive plans on the market covering:

- Wills & Trusts

- ID Monitoring

- Divorce

- Consumer Protection

- Criminal Defense

- And Much More

With a vast network of licensed attorneys across the State of Texas, our members have access to the best legal help without the high price tag.

For more information, click on the plan summaries below.

401(k)

Fidelity Customer Service | (800) 835-5097 | www.401k.com

No matter what point of your career you’re in, it’s never a bad time to think about your future and save for retirement

Employees who take advantage of their employer-sponsored retirement plan and commit to saving for their future have the advantage of improving their financial security in retirement. Think of your plan as insurance for your income when you are no longer working!

More about your 401(k) Plan

- With our retirement plan, you can save for your future-self by contributing to either the Traditional (pre-tax), Roth (after-tax), or both options! Whichever tax-advantaged strategy you decide on, the earlier you begin, the more time your assets will have to grow.

- MedeAnalytics is pleased to offer a 50% match on your contributions, up to 6% of your salary. This means that by saving for your retirement, you can take advantage of this generous matching program and boost your savings even further. To get started, set up your account with Fidelity by visiting www.401k.com or calling 1-800-835-5097 to begin contributing to your plan immediately upon your date of hire

Pre-tax vs. Roth 401(k): What’s the difference between Traditional (pre-tax) and Roth (after-tax) contributions?

- The distinction lies in how they are taxed each pay period, their impact on your annual taxable income when filing, and distribution at retirement. With the Traditional 401(k), the money you contribute is not taxed until you withdraw it at retirement. On the other hand, the Roth option requires you to pay taxes on the money you contribute. The advantage of the Roth is that you can withdraw your distributions tax-free during retirement

Contributing to the Plan

- The IRS sets the deferred contribution limit annually, and for 2024, it is set at $23,000. If you’re aged 50 or older this year and have already maximized your contributions, you can accelerate your progress towards your retirement goals by making a “catch-up contribution.” In 2024, the maximum catch-up contribution is $7,500, bringing your combined total contribution allowance to $30,500. These contribution limits are indexed to inflation and subject to change each year. Contact HR for the most current contribution limits.

CARRIER CONTACTS

As you consider your benefit options, please be sure to review all available information summaries and other videos and flyers found on this webpage. Click on the document below to see important contact information.

[INSERT CARRIER CONTACTS]

MEDICARE ELIGIBLITY

Medicare eligibility is a critical aspect of healthcare planning, particularly for individuals nearing age 65 or those with qualifying disabilities. Here are the key points to keep in mind:

- **Age 65 or Qualifying Disability**: Most individuals become eligible for Medicare at age 65, while those with certain disabilities or medical conditions may qualify earlier.

- **Comprehensive Coverage**: Medicare provides coverage for hospital stays, medical services, prescription drugs, and preventive care, offering essential healthcare benefits.

- **Enrollment Periods**: It's important to understand the various enrollment periods for Medicare, including the initial enrollment period, special enrollment periods, and annual open enrollment periods for making changes to coverage.

- **Supplemental Coverage Options**: Many individuals choose to supplement their Medicare coverage with additional plans, such as Medicare Advantage (Part C) or Medicare Supplement Insurance (Medigap), to enhance benefits and fill gaps in coverage.

As you navigate your benefit elections, be sure to consider your Medicare eligibility and options alongside your employer-provided benefits. Understanding your Medicare coverage can help ensure comprehensive healthcare coverage that meets your needs as you transition into retirement.

- Premium: The amount paid for insurance coverage deducted from your paycheck on a per-pay-period basis.

- Deductible: The amount you must pay out of pocket for covered services before your insurance plan starts to pay.

- Copayment (Copay): A fixed amount you pay for covered services at the time of service, usually for doctor visits or prescription drugs.

- Coinsurance: The percentage of costs you pay for covered services after you've met your deductible.

- Out-of-Pocket Maximum: The maximum amount you'll have to pay for covered services in a plan year, after which your insurance plan pays 100% of covered costs.

- Network: The group of doctors, hospitals, and other healthcare providers contracted with an insurance company to provide services at discounted rates to plan members.

- Preventive Care: Healthcare services aimed at preventing illness or detecting health conditions early when treatment is most effective, often covered at no cost under insurance plans.

- Benefit: The healthcare services or items covered by an insurance plan.

- Preauthorization: The process of obtaining approval from your insurance company before receiving certain medical services or treatments.

- In-Network: Healthcare providers or facilities that have contracted with your insurance company to provide services at lower costs to plan members.

- Exclusion: Specific healthcare services or conditions that are not covered by an insurance plan.

- Lifetime Maximum: The maximum amount of money that an insurance plan will pay for covered services over the entire life of the policy.

- Grace Period: A specified period after the premium due date during which coverage remains in force even though the premium has not been paid.

- Coordination of Benefits (COB): A process used when an individual is covered under more than one health insurance plan to determine which plan pays first and how much each plan will pay.

- Explanation of Benefits (EOB): A statement sent by the insurance company to the insured individual explaining what medical treatments and/or services were paid for on their behalf.

REQUIRED NOTICES

Federal regulations require employers to provide certain notifications and disclosures to all eligible employees. The booklet linked below is dedicated to those disclosures for 1/1/2025 – 12/31/2025. If you have any questions or concerns please contact your HR Department.

If you (and/or your dependents) have Medicare or will become eligible for Medicare in the next 12 months, a Federal law gives you more choices about your prescription drug coverage. Please see page 4 of the Required Notices packet for more information about your options.

Why go to an In-network provider?

- Going to an in-network provider means choosing a healthcare professional or facility that has a contract with your health insurance plan. In-network providers have agreed to offer their services at negotiated rates, which are often lower than what you would pay for out-of-network care. By visiting an in-network provider, you can take advantage of your health insurance plan's benefits, which may include lower copayments, coinsurance, and reduced out-of-pocket expenses.

Why should I go for my annual well checkup?

- Annual well checkups are essential for maintaining good health and preventing potential health issues. These visits allow your doctor to assess your overall health, monitor any chronic conditions you might have, and detect early signs of potential health problems. Regular checkups help identify health concerns before they become serious, ensuring timely intervention and a better chance for successful treatment.

What is the difference between generic and brand name drugs?

- Generic drugs are identical or bioequivalent to brand-name drugs in terms of active ingredients, safety, strength, dosage form, and intended use. The main difference is that generic drugs are usually more affordable because they don't have the research and development costs associated with brand-name drugs. The U.S. Food and Drug Administration (FDA) ensures that generic drugs meet the same rigorous standards for quality, safety, and effectiveness as their brand-name counterparts.

How do discount cards work on RX?

- Prescription discount cards provide discounts on medications at participating pharmacies. These cards are often available for free or at a low cost and can be used by individuals without insurance or those with high copayments. When you present the discount card at the pharmacy, it reduces the price of the medication, potentially leading to significant cost savings.

What happens if I go out of network?

- If you go out of network for healthcare services, it means you're seeing a provider or using a facility that doesn't have a contract with your health insurance plan. Out-of-network care typically results in higher out-of-pocket costs, including higher copayments, coinsurance, and potentially higher deductibles. Some health insurance plans may not cover out-of-network care at all, except in emergencies.

What is a SBC (Summary of Benefits and Coverage)?

- A Summary of Benefits and Coverage (SBC) is a document provided by health insurance companies to help individuals understand their health plan's key features and coverage details. It provides a summary of the plan's benefits, costs, coverage limits, and examples of common medical scenarios to help individuals compare different health insurance options and make informed decisions.

What is an EOB (Explanation of Benefits)?

- An Explanation of Benefits (EOB) is a statement sent by the health insurance company to the policyholder after a healthcare claim has been processed. The EOB provides a detailed explanation of the services provided, the amount billed by the healthcare provider, the amount covered by the insurance, and any remaining balance that the insured may be responsible for paying.

What should I ask my doctor?

- When visiting your doctor, consider asking questions related to your health condition, treatment options, medications, potential side effects, and any lifestyle changes you should make. You can also inquire about preventive measures, recommended screenings, and follow-up care. Don't hesitate to ask for clarification if there's anything you don't understand.

What is preventive care?

- Preventive care refers to healthcare services aimed at preventing or detecting health issues before they become more severe or chronic. Examples of preventive care include vaccinations, screenings (e.g., mammograms, colonoscopies), regular checkups, counseling on healthy behaviors, and interventions to manage risk factors.

Where can I get my ID card?

- You can typically get your health insurance ID card from your insurance provider. Many insurers offer electronic versions of the ID card through their mobile apps or member portals. Alternatively, you can request a physical ID card to be mailed to you.

Who do I contact if I have a QLE (Qualifying Life Event)?

- If you experience a Qualifying Life Event (QLE), such as marriage, birth/adoption of a child, divorce, loss of other health coverage, or a change in household income, you should contact your employer's HR department or your health insurance provider promptly. They can guide you through the process of updating your health insurance coverage or enrolling in a new plan if necessary.